The multipurpose shipping market is not expected to recover until the end of 2017, when it is anticipated that there will be more bulk demand for the Handy vessels and therefore more breakbulk cargoes for multipurpose vessels, according to the latest Multipurpose Shipping Market Review and Forecast 2016 report published by global shipping consultancy Drewry.

Damen multi-purpose vessel design Combi Freighter 8200 "Onego Arkhangelsk" Image: Damen

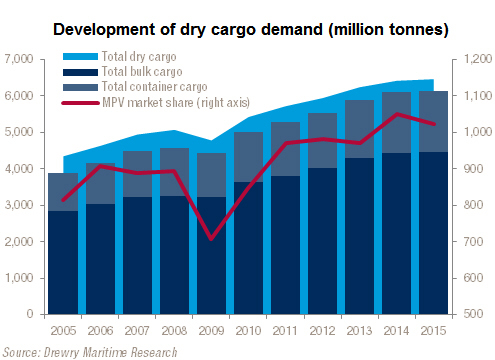

The last 12 months have been dreadful for the multi-purpose vessel (MPV) market with rates at rock bottom and competition for cargo from every angle. Weak demand, coupled with falling commodity prices and the oversupply of tonnage in competing sectors has brought rates down to levels not seen since just after the global financial crisis. The demand for multipurpose shipping registered a drop of almost 3% in 2015 as global demand for dry cargo slowed considerably while competition for it increased. The main competition faced by the MPV sector comes from Handy bulk carriers and containerships. The market for the first finished 2015 on its knees with earnings less than half the operating costs for the vessels, whilst the container lines were offering rates at close to zero just to hang on to market share.

Going forward, dry cargo growth is set to improve in 2017 and beyond but the return to growth for the MPV market share will be almost entirely dependent on the competing sectors. Whilst we are confident that both breakbulk and project cargo demand are showing signs that, in the medium term at least, volumes will return to growth trends, we are not confident that the competing sectors will move back to their more traditional cargoes anytime soon. The container market, however, is not expected to show any improvement for two and possibly three years. It is likely that containerships will continue to aggressively target breakbulk and project cargo for the foreseeable future.

In order to estimate the effective demand for the MPV fleet, we assess the demand for all possible commodities and the modal split for these between bulk, breakbulk and container. Susan Oatway, lead analyst for multipurpose shipping comments:

“We expect the effective demand for the MPV fleet to return to a positive trend with average annual growth of 2.7% to 2020. However, this growth will be very subdued through 2016 and will not show any significant improvement until the end of 2017. This is due to a combination of the lack of project finance and aggressive competition from the container and Handy bulk carrier sectors. ”

The supply of multipurpose vessels to carry this cargo is growing very slowly as well. Drewry has assessed future newbuilding deliveries, potential demolition candidates and slippage at the yards to determine that the future fleet will grow at less than 0.5% a year to 2020. However, more interestingly, the project carrier fleet is expected to grow at almost 4% a year, whilst the ‘simple’ MPV fleet will contract at a rate of almost 3% a year. Owners have borne untenable market conditions for longer than expected but now there is a very real risk for the financial stability for a number of companies.

“All this suggests that for those that can survive 2016 and position themselves with unique qualities – whether that is financial stability, good management, eco-friendly engines or extraordinary lift – there is an end to this recession. While we do not see any sign that, even in the longer term, the market will return to pre-2009 levels, it should see enough improvement to recover to 2011 levels by the end of our current forecast period,” added Oatway.

Source: Drewry