The rise of deepwater E&P constituted a boon for the offshore fleet, helping to drive, for example, 180% and 60% increases in the FPSO and floater fleets from 2000 to 2015. However, deepwater development has lagged exploration, and so the offshore sector is fairly exposed to projects with high breakevens – problematic, given the oil price. But could the downturn actually help deepwater E&P in the long term?

Deepwater Exploration

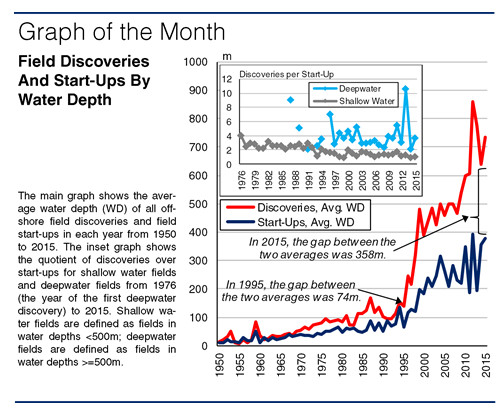

The first deepwater offshore discovery was not made until 1976, by which point 1,018 shallow water fields had been discovered and 350 brought onstream, and it was only in the late-1990s that deepwater E&P really took off. Oil companies began pushing deeper into the US GoM, while the internationalization of the industry in the 2000s saw a spate of deepwater discoveries off West Africa and Brazil. A robust and rising oil price helped sustain rising deepwater E&P until 2015, with India, Australia and East Africa becoming important frontiers too. The average water depth of global offshore field discoveries passed 200m for the first time in 1996, 500m in 2004 and 800m in 2012, and the number of deepwater discoveries averaged 55 per year from 2005 to 2015.

Deepwater Production

However, as the main graph shows, the mean water depth of discoveries rose much faster than did that of start-ups: the former stood at 734m in 2015, the latter at 377m. Indeed, by 2016, out of a total of 998 deepwater finds, just 27% had started up, with deepwater start-ups averaging 19 per year from 2005 to 2015. The divergence was in large part because technological barriers and cost overheads in deepwater production – subsea, SURF and MOPU – are more complex and expensive than in exploration, and efficiency gains seem to have been more limited to date as well. Deepwater project sanctioning was therefore relatively inhibited, and due to limited sanctioning, the backlog of undeveloped deepwater fields grew at a faster rate than that of shallow water fields, as indicated by the inset graph. Thus over time, the overall backlog of potential projects has become more costly and complex. Indeed, some reports suggest oil project average breakevens have risen by c.270% since 2003.

Deepwater Challenges

This is partly why the offshore outlook is challenged at present: deepwater fields have relatively high breakevens (usually $60-$90/bbl) yet also form a major part of oil companies’ portfolios. Some major oil companies have indicated that 2016 E&P spending cuts are to bite deeper off than onshore, where costs are lower (even for shale, in many cases). In January 2016, Chevron decided to axe outright Buckskin, a US GoM project in a water depth of 1,816m with a breakeven of c.$72/bbl. ConocoPhilips, meanwhile, is planning to exit deepwater altogether.

However, in order to make deepwater viable again, many companies are trying instead to cut project costs. Statoil, for example, has reduced the CAPEX of Johan Castberg by 48% and the breakeven by 40%. Some cost savings (in day rates, for instance) are likely to be cyclical; others, such as in subsea fabrication, yielding improved deepwater project economics, are likely to be more lasting. So while exposure to deepwater projects is clearly a challenge given the current oil price, cost cutting now could be to the benefit of deepwater E&P in the long run.

Source: Clarkson Research Services Limited